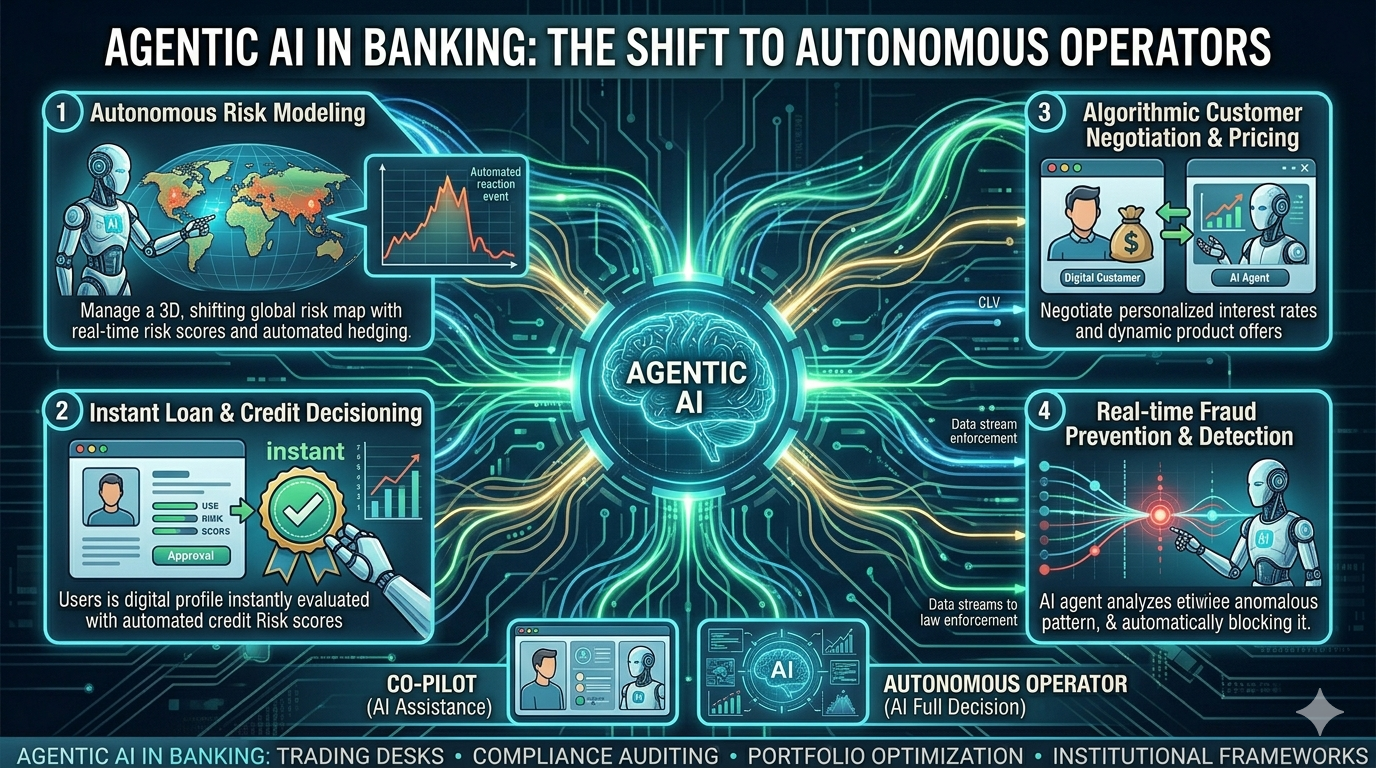

From Co-Pilots to Autonomous Operators: The Rise of Agentic AI in Banking

If 2024 and 2025 were defined by generative AI experimentation, 2026 is officially the year of execution.

For the past two years, artificial intelligence in the financial services sector was primarily an exercise in conversational assistance. We saw a massive influx of customer-facing chatbots, internal search tools, and AI co-pilots designed to help human operators summarize data slightly faster.

But over the last quarter, a massive paradigm shift has swept through the fintech landscape. The industry is moving away from basic text-in, text-out assistance and aggressively deploying Agentic AI into production.

According to recent data from Wolters Kluwer, nearly 44% of global finance functions are actively integrating agentic workflows this year—a massive 600% increase compared to early pilots. The narrative has completely evolved: we are no longer just building tools that talk to humans; we are building autonomous software agents engineered to reason, make decisions, and execute multi-step workflows across legacy financial networks.

What Makes Agentic AI Fundamentally Different?

To understand why global institutions are pouring billions into agentic frameworks, we have to look at how the technology operates compared to standard large language models (LLMs).

Traditional banking chatbots are reactive. They rely on pre-defined rules or semantic search indexes to pull answers from an internal database. If a user asks a legacy chatbot to resolve a billing dispute, the bot can do little more than surface a policy document or write an automated reply script.

Agentic AI is proactive and execution-oriented. An AI financial agent doesn't just read data—it uses a dynamic loop of planning, reasoning, and system tool execution to solve abstract problems from start to finish.

[Legacy Chatbot] ───► "Here is the PDF policy for filing a transaction dispute."

[Agentic System] ───► Ingests Dispute ───► Audits Ledger ───► Verifies Identity (KYC) ───► Executes Settlement

When an agentic system encounters a transaction dispute, it follows a completely autonomous chain of logic:

It calls an API to ingest the transaction history.

It reasons through potential merchant fraud parameters using real-time behavioral biometrics.

It cross-checks the user's historic compliance logs via internal data clean rooms.

It executes the micro-settlement directly on the payment rail without requiring manual data entry from a human manager.

Production Use Cases Dominating FinTech Right Now

Fintech enablers and horizontal software providers are rapidly deploying multi-agent systems that cross-examine each other's work to handle high-stakes financial operations.

1. Embedded Anti-Money Laundering (AML) Investigations

Manual compliance mapping has historically been one of the costliest bottlenecks in commercial banking. Industry data from Ernst & Young (EY) reveals that deploying agentic AI platforms to handle deep AML research has resulted in a 50% time reduction per investigation, effectively saving hours of heavy manual data stitching per background file.

2. Autonomous Credit Underwriting

Instead of checking standard credit bureau filings once a month, autonomous risk engines utilize alternative data swarms—such as real-time cash flow vectors, digital utility payments, and mobile transaction behaviors—to build dynamic, live risk scores. These agentic layers can safely automate loan routing and credit extension for thin-file applicants under highly localized market fluctuations.

3. Hyper-Personalized Wealth Management

Instead of static portfolio models, specialized wealth agents are running 24/7 background simulations on global market movements, tax efficiencies, and individual liquidity needs. These agents can proactively flag structural asset rebalancing opportunities, reducing manual prospecting time for investment advisors by up to 40%.

The Strategic Caveat: Governance is the Real Moat

While the efficiency gains are undeniable—with research indicating that companies see an average return of $3.50 for every $1 invested in autonomous agent frameworks—the transition to autonomy introduces severe legal risks.

Speed without precise explainability is an existential regulatory liability under modern compliance acts like the EU AI Act and DORA. Because agentic systems can chart their own multi-step operational paths, they can introduce complex failure modes that standard rule-based software never encountered.

If an AI agent autonomously rejects a loan or freezes a merchant account without keeping a clear, human-readable audit log of its reasoning path, the financial institution faces immediate regulatory exposure.

GOVERNED AGENTIC EXECUTION ENVIRONMENT

┌──────────────────────────────────────────────────┐

│ │

│ [Live Data Inputs] ───► Context Engine │

│ │

│ [Dynamic Reasoning] ───► Semantic Trust Layer │

│ │

│ [API Execution] ───► OpenTelemetry Audit Log │

│ │

└──────────────────────────────────────────────────┘

The fintechs pulling ahead are not simply deploying raw, open-source models out of the box. They are building governed execution environments that rely on standardized protocols (like the Model Context Protocol) to restrict an agent's tool access, enforce strict operational guardrails, and generate permanent OpenTelemetry-compliant tracing maps for human review.

The Bottom Line

A feature is no longer a fintech. As financial capabilities become exposed as machine-grade services and payments move toward real-time, instant settlement rails, the competitive advantage belongs to those who control the orchestration layer.

The banks and fintech platforms that succeed in this new era will be the ones that completely dismantle their disconnected data silos and construct a fluid ecosystem where autonomous agents can operate securely, transparently, and with absolute accountability.